Dollar Weaponisation and Family Finance: Why Muslims Need a Backup Plan

Dollar Weaponisation and Family Finance: Why Muslims Need a Backup Plan

When British Muslims think about their family finances, the focus is usually on mortgages, pensions, student loans, or the monthly bills that never seem to stop rising. Few pause to consider how global currency politics affects those same finances. Yet the truth is simple: sterling, for all its history, is tied at the hip to the US dollar. When Washington makes a move, London follows. And when the dollar is weaponised, as it has been repeatedly, British families feel the consequences --- whether through higher prices, restricted financial flows, or instability that eats into savings.

For Muslim families in the UK, this reality matters in more ways than one. It affects not only the cost of living but also the ethical dimension of where our money sits and how dependent we are on systems that work against the Ummah. Understanding dollar weaponisation isn't just for economists. It's a survival issue for ordinary households.

What Dollar Weaponisation Means

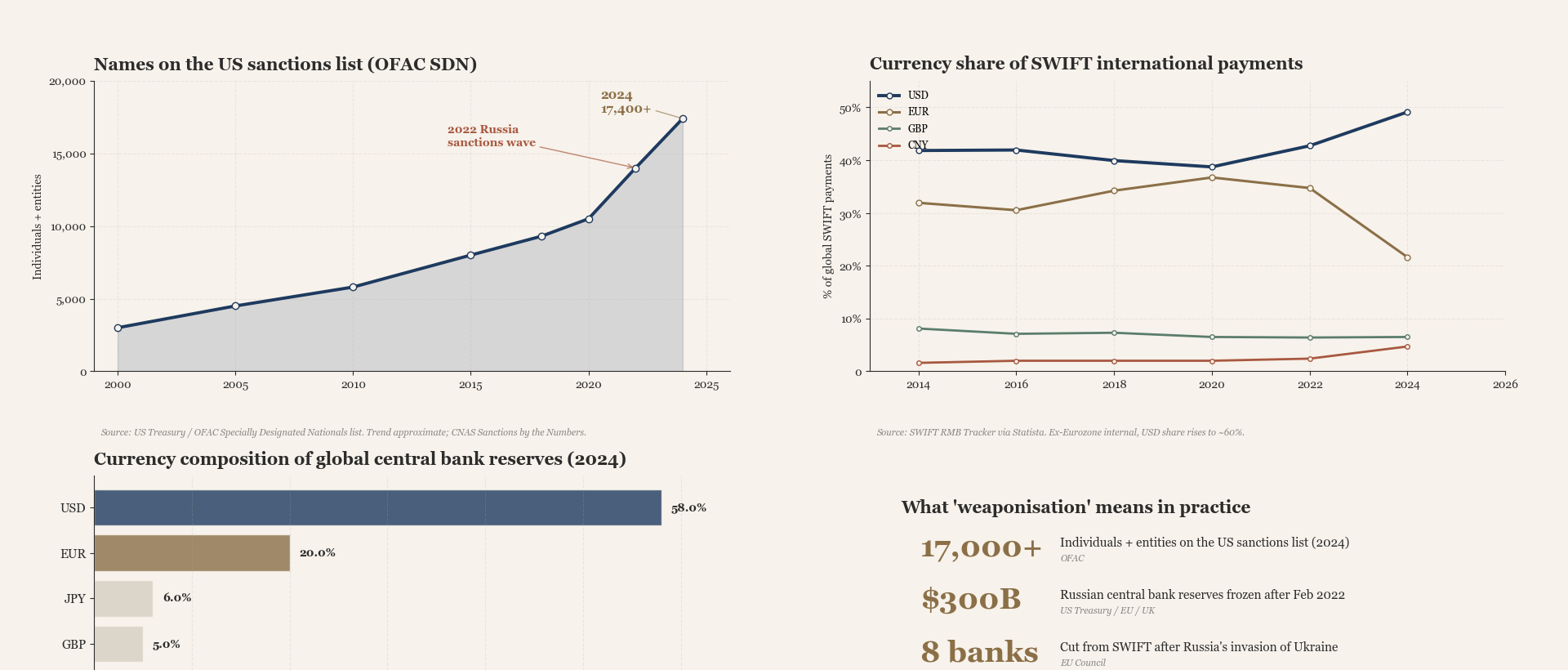

The dollar has been the backbone of the global financial system since the mid-20th century. Around 60% of global reserves and 80% of trade are conducted in dollars. This dominance allows the US government to use the currency as a political tool.

We've seen it clearly:

- Freezing of central bank reserves, such as Afghanistan's and Russia's.

- Sanctions cutting entire countries out of the banking system.

- Surveillance that slows or blocks Muslim charities, remittances, and

even family transfers.

This is what "weaponisation" means: using currency not as neutral money, but as leverage to punish, coerce, and control.

Why This Matters in Britain

At first glance, Britain feels insulated. We don't use dollars at the supermarket. But sterling is deeply linked to the dollar system. Oil and gas are priced in dollars. Global commodities from wheat to metals are traded in dollars. British banks rely on dollar clearing.

This means:

- Energy bills rise when dollar markets tighten.

- Food prices climb when global trade routes are disrupted.

- Banking gets tighter when US-driven compliance rules target Muslim

charities or individuals.

So even without holding a dollar, British Muslim families feel its power.

The Ethical Dimension

There is another layer: complicity. When our wealth is tied into systems dominated by the dollar, we indirectly participate in its use against Muslim countries. Taxes, pensions, and investments often end up funding the very powers that sanction and destabilise Muslim lands. This doesn't mean we can abandon sterling overnight, but it does mean recognising the moral stakes in how dependent we are on Western financial structures.

Islamic Anchoring

Islam places wealth within a moral framework. "Do not consume one another's wealth unjustly" (Qur'an 4:29). Systems that use money as a weapon against the weak fall into this warning. The Prophet ﷺ reminded us that wealth is a trust, and misuse leads to loss of barakah. Foresight in finances is therefore not only practical but spiritual.

Case Study: The Ahmed Family in London

The Ahmeds run a small business and send money regularly to relatives abroad. After sanctions tightened on certain regions, their transfers were delayed for weeks, with banks demanding endless paperwork. At the same time, rising energy bills ate into their profits, and sterling's weakness after global shocks reduced their savings power.

Frustrated, they looked at diversifying. They began by buying a modest apartment in Istanbul. This gave them a foothold in a market less tied to sterling's swings, allowed them to keep part of their savings in lira and gold, and created a safe haven for the family. They still live in London, but they no longer feel completely captive to a single system.

Practical Implications for Families

- Remittances: Expect more scrutiny, delays, and costs as US

oversight intensifies. Families should prepare alternative channels where possible.

- Savings: Keeping all assets in sterling exposes families to

inflation and currency decline.

- Charity: UK Muslims who support causes abroad will increasingly

face compliance checks. Planning ahead matters.

- Employment: British industries dependent on global trade and

finance are vulnerable to dollar shocks. Job security cannot be taken for granted.

The Second Home Bridge

For many families, the simplest diversification is physical: a second home abroad. This doesn't mean abandoning the UK. It means reducing dependency. A property in Turkey, Malaysia, or the Gulf can:

- Store wealth in a different currency environment.

- Provide an asset that remains valuable even if sterling weakens.

- Serve as a practical refuge if financial restrictions tighten.

Even families not ready for Hijrah can benefit. Just as investors diversify portfolios, Muslims can diversify their futures.

Britain's Fragile Position

The UK is already struggling with inflation, rising debt, and declining competitiveness. Tied to the US economically, it inherits both the strengths and weaknesses of the dollar system. As BRICS+ countries work to trade in local currencies, the dollar's dominance may weaken. But in the short term, that process will create turbulence. Families anchored only to sterling will feel exposed.

Conclusion

Dollar weaponisation is not an academic concern. It is a lived reality for Muslim families in Britain, shaping bills, savings, remittances, and opportunities. It is also a moral concern, tying us to systems that harm the Ummah.

The solution is not panic, but foresight. Strengthen financial resilience, diversify assets, and build bridges abroad. For many, that will mean considering a second home or base in the Muslim world. Not as a luxury, but as a safeguard --- spiritual, financial, and practical.

In an age when money itself is used as a weapon, Muslims cannot afford to be naïve. We owe it to our families to prepare, and to our deen to ensure our wealth remains a source of barakah rather than burden.

What your family can do now

You do not need to become a financial expert. But you can take practical steps:

- Hold some of your savings in gold or property rather than purely in cash.

- Reduce reliance on sterling by building assets in other currencies or countries.

- Review whether your pension and investments are fully exposed to the dollar system.

- Use Islamic finance alternatives where available — they are growing.

- Explore whether a second home or residency abroad could diversify your family's risk.

Next Step: The practical question that follows is: where do you diversify? [The Second Home Strategy](../article/the-second-home-strategy) and [Zakat, Taxes, and Residency](../article/zakat-taxes-and-residency-navigating-your-obligations-abroad) both offer grounded next steps for families building financial resilience beyond the dollar system.